Interesting performance can be seen now days in treasury

yields versus the S&P 500. While the S&P 500 moves sideways at

increasing heights, yields of treasuries are beating stock performance. Keep in

mind that demand in treasuries, or bonds in general, drive up their price,

which decreases their yield--as a matter of convention. Stocks simply climb or go down.

Stocks have been climbing to 4 year highs, or moving sideways

until their next move higher. And Treasury bonds have also been climbing in yield, but

at stronger rates than stocks.

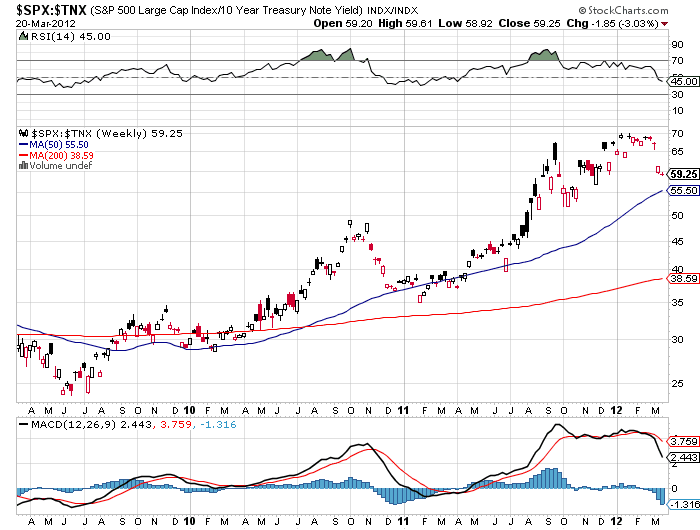

Based on the chart above, S&P 500 stocks are compared with 10

year Treasury Note yields. Stocks have been under performing considerably since

the later part of February. This occurrence is of thoughtful note in that stock

prices have remained strong, alongside greater momentum in U.S. bond yields.

Typically, and for some time, treasuries are safety nets

where stock returns are a risk-on asset class. This means that when the market

gets insecure, stocks fall and treasury prices increase. The reverse occurs when the

market is secure and feels that more risk is warranted. Otherwise spoken,

stocks and treasury prices typically trade inversely to each other.

Now, stocks are holding strong, when treasury yields are finding

greater strength. Causes for both asset classes holding strength can

perhaps be found in demand for U.S. bonds as a form of banking collateral.

Evidence can be seen not only in the 10 year note, but also the 30 year bond, demonstrated above.

Week before last, I made comment on the Fed’s proposed

reverse repurchase operations. Operations of this nature involve the fed

lending its collateral of treasuries in exchange for deposits at its location.

Net results are dollar values flooding across the globe, lead by loans of treasuries.

Ultimately, the U.S. dollar underperforms as with

conventional forms of quantitative easing. Currently, where we see sustained

equity prices but not major increases, and strong performance in treasury yields, we are also seeing the dollar

underperforming equities. Usually, the dollar will rise in association with

increases in treasury prices, while equities decline. Now while equities stay level, and

treasuries yields spike, the dollar under performs. For example, compare the dollar against the S&P 500 in the chart.

Look for example at the performance of the dollar against the 10 year treasury note yield below.

It does appear that demand for treasury securities has

increased considerably, without the typically expected decline in equities--and especially the increase in treasury pricing.

Still, the dollar is underperforming equities and treasury yields. Dollar

performance, amid the other named dynamics, tells of increased U.S. dollar

availability or U.S. asset availability.

Now, it does appear that U.S. treasuries are supporting values

of international banking collateral. Causation for this proposition is through the reverse repurchase agreement.

Essentially the party, or primary dealer, loaning the treasury to a foreign bank counter-party will want to lend the treasury at a higher price than the price at which the lending party will have to buy-back the treasury. Ergo, lend at high prices, to buy back at low prices. Yields, being inverse, also support the lender by increasing at buy back time, when yields are higher and prices lower.

Dynamics of this nature are perhaps risky due to the ECB’s existing exposure to various European bonds. While strong collateral is bought by international banks at decreasing prices, but increasing yields, look at the overall price/yield consequence to be absorbed by European sovereign bonds.

Propositions for sovereign bond consequences is that their prices could continue to fall, and yields rise. All contrary to realizing expected results of increasing the credit ratings of bank collateral.

Essentially the party, or primary dealer, loaning the treasury to a foreign bank counter-party will want to lend the treasury at a higher price than the price at which the lending party will have to buy-back the treasury. Ergo, lend at high prices, to buy back at low prices. Yields, being inverse, also support the lender by increasing at buy back time, when yields are higher and prices lower.

Dynamics of this nature are perhaps risky due to the ECB’s existing exposure to various European bonds. While strong collateral is bought by international banks at decreasing prices, but increasing yields, look at the overall price/yield consequence to be absorbed by European sovereign bonds.

Propositions for sovereign bond consequences is that their prices could continue to fall, and yields rise. All contrary to realizing expected results of increasing the credit ratings of bank collateral.

Still, there are likely few

alternatives in the effort to support banking health.

No comments:

Post a Comment